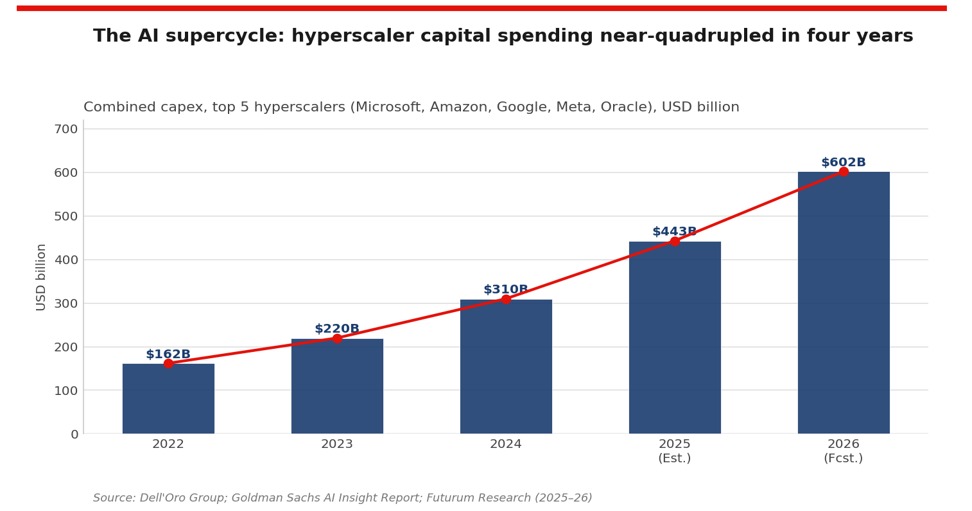

We are witnessing one of the biggest infrastructure buildouts in our lifetime. The numbers are staggering. Global hyperscalers — Microsoft, Amazon, Google, Meta, and Oracle — are expected to spend over $600 billion on capital expenditure in 2026 alone, a 36% jump from 2025. About 75% of that is going into AI infrastructure: chips, servers, and the buildings that house them. Data centre capex globally is heading past $1 trillion by 2030.

The US Is Drowning in Its Own Success

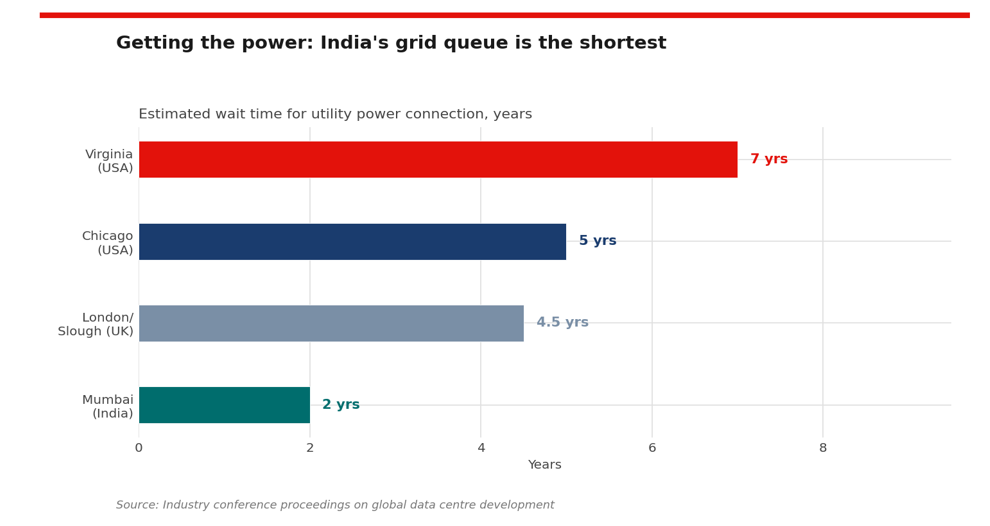

Here is the paradox at the centre of this story. The country that created AI — the United States — cannot build fast enough to meet its own demand. US data centre capacity stands at roughly 37–40 GW today. Getting a new power connection in Virginia, the world’s largest data centre hub, takes up to seven years. In Chicago, five years. Even in outer London, you are looking at four to five years for a grid connection. Global data centre occupancy is running at 97%. There is simply no room.

The US grid cannot absorb the demand. Companies are now locating gas pipelines, tapping on-site supply, and building power generation facilities before they build the data centre. Meta has announced a 5 GW cluster in Louisiana. Elon Musk’s xAI pushed through a gigawatt-scale cluster in months using extreme workarounds. The lesson: power, not land or capital, is the binding constraint.

And this is where India comes in. Mumbai is offering power connections in around two years — a fraction of what US developers are dealing with. India has 260+ GW of non-fossil power already installed, added a record 44.5 GW of renewable capacity in 2025 alone, and is targeting 500 GW by 2030.

India’s Data Centre Story: From Backwater to Boom

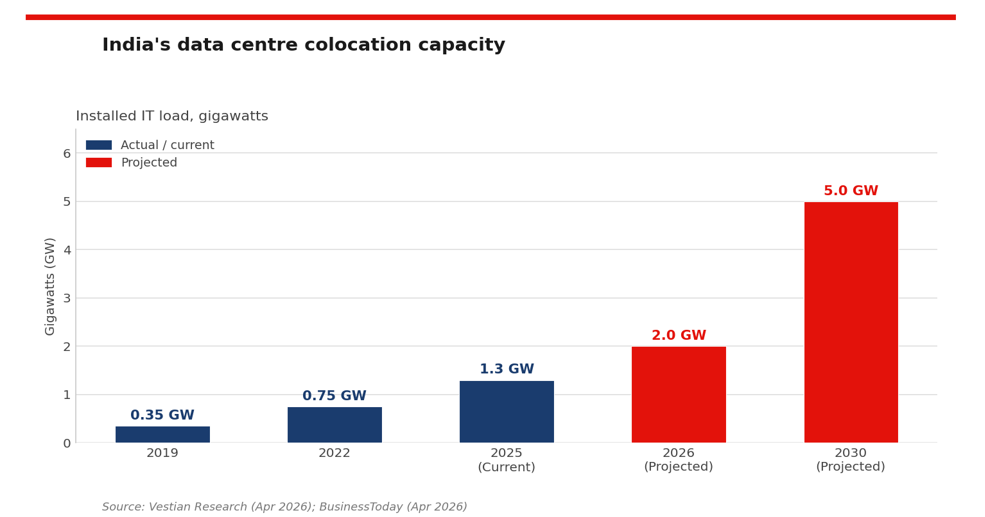

India’s data centre journey has been quiet but relentless. In 2019, total colocation capacity was around 350 MW. Today it stands at approximately 1.3 GW — nearly a fourfold increase in six years. By the end of 2026, projections put us at 2 GW, backed by $30 billion in committed investments. The longer-term target is 5 GW by 2030 under base-case scenarios, with AI-accelerated upside scenarios pointing toward 8–9 GW.

What changed? Three things happened roughly simultaneously.

Hyperscalers arrived and started building availability zones.

The mobile revolution brought hundreds of millions of Indians online.

And cloud adoption took off — growing at 20–30% year-on-year, effectively doubling every three to four years. That created the base demand. AI is now the second layer on top of an already-accelerating trend.

The geography of India’s data centre market is also becoming clearer. Mumbai — and specifically Navi Mumbai — is the epicentre for hyperscale and enterprise colocation, driven by existing digital infrastructure and financial sector demand. Vizag is emerging as the hub for large AI training clusters, with Google committing to build what would be the largest AI hub outside the US there. Hyderabad and Chennai are adding capacity fast. The market is no longer a Mumbai-only story.

The Cost Advantage is Structural

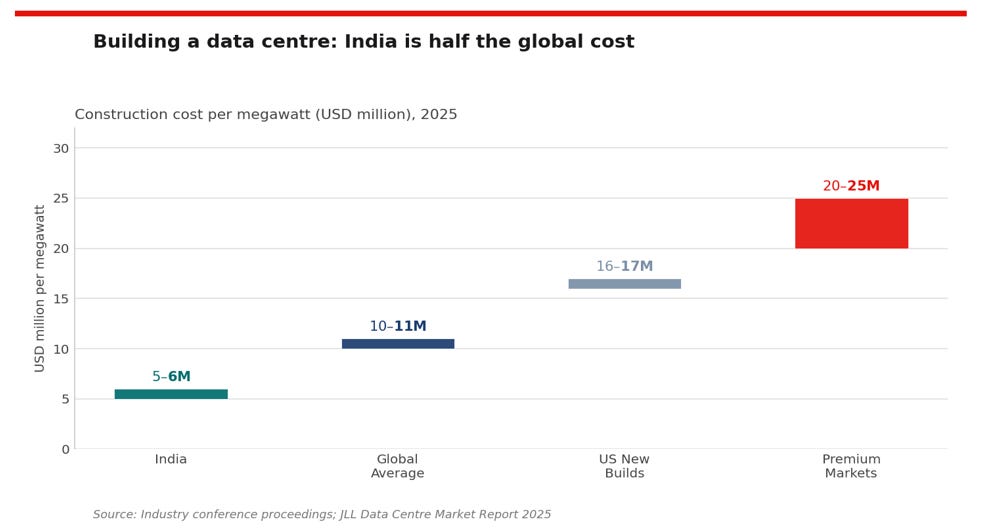

People often ask me why global operators are choosing India over Southeast Asia or Eastern Europe. The answer is partly cost, and the numbers make the case plainly.

Building a data centre in India costs roughly $5–6 million per megawatt — including land preparation, substations, buildings, generators, and fit-out. The global average is $10–11 million per megawatt. In the US, new projects that were being planned at $14–15 million per megawatt are now trending toward $16–17 million as supply-chain inflation bites. Premium US and European markets can reach $20 million or more.

That cost gap is not closing. US construction costs are rising as the buildout accelerates and supply chains strain. India’s cost advantage — in land, labour, civil construction, and increasingly in power — is increasing.

And then there is the geopolitical argument. In a world where companies are being asked to diversify away from concentration risk in any single geography, India is viewed as a credible, non-adversarial alternative. Not anti-US, not under sanctions risk, not politically unpredictable. That positioning is quietly worth a lot.

The Capital is Already Here

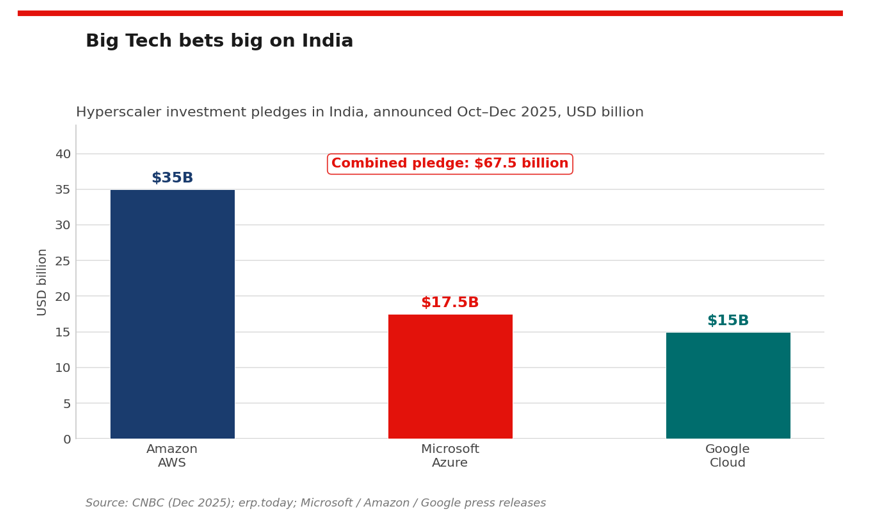

Between October and December 2025, three hyperscalers announced investment commitments to India that added up to $67.5 billion. Let that sink in. In a single quarter. Amazon pledged $35 billion, Microsoft $17.5 billion, and Google $15 billion. These are not MoU-level pledges — these are backed by specific site acquisitions, land purchases, and build-to-suit contracts already in motion.

Institutional capital is moving with equal conviction. BlackRock has done a $48 billion acquisition of Aligned Data Centers in the US. Blackstone paid a $16 billion equity cheque for AirTrunk in Asia. KKR has been in discussion for STT at an estimated $10 billion equity cheque. The data centre sector is now attracting the kind of capital that used to flow into real estate and infrastructure funds — because that is effectively what it has become.

India is not immune to this. Blackstone’s India platform Lumina has already been acquired by a different Blackstone fund. The industry is watching the upcoming Sify Infinit Spaces IPO — the first SEBI-approved data centre IPO in India at INR 3,700 crore — very closely. Nxtra Data (Airtel’s data centre arm) has filed its DRHP. Yotta Infrastructure is planning to list in FY2026–27. CtrlS has a $2 billion capex plan in motion.

The IPO market for data centres is about to open up. And the valuation benchmarks that get set in these first listings will define the opportunity for years.

The Global Supercycle: Context for Indian Investors

Big Tech AI capital expenditure has grown from $162 billion in 2022 to an estimated $443 billion in 2025 — a near-3x in three years. Goldman Sachs projects that hyperscalers will spend $1.15 trillion between 2025 and 2027. Global data centre infrastructure spending is heading toward $1 trillion by 2030. These are railroad-scale numbers. The comparison to America’s 19th century railroad buildout is not hyperbole — it is the most accurate historical analogy available.

AI workloads could account for half of all global compute by 2030. And the demand is evolving. Today it is mostly about training large models in giant centralised clusters. Tomorrow it will be about inferencing — running AI at the point of use, in city-level data centres, in enterprise deployments, at the edge. That inferencing demand will be more distributed, and countries like India with strong enterprise bases and large digital populations will be natural beneficiaries.

Every electric vehicle on the road, every connected security camera, every bank running AI on its customer data — all of it needs compute. The demand story does not depend on a single application succeeding. It is structural.

The Risks Are Real Too

I would be doing you a disservice if I did not flag the risks clearly.

· Power supply bottlenecks: Mumbai’s 2-year connection timeline will worsen as absorption accelerates. Developers need to price in power risk just as much as land risk.

Water consumption: A 5 GW data centre industry in India by 2030 could consume over 350 billion litres of water annually. Cooling is water-intensive. This is a real environmental and regulatory risk, especially in water-stressed regions.

Community acceptance: National policy may support data centres, but local opposition — on grounds of radiation fears, industrial encroachment, or land use — is a genuine constraint. We have seen this in France and the US. India is not immune.

Supply-chain pressures: Generator sets are on 18-month lead times. Server costs in some configurations have risen 5x in 10 months. Equipment delays can stall projects that are otherwise ready to go.

Valuation discipline: When the first data centre IPOs list at high multiples, there will be a temptation to chase. The business quality varies significantly between operators. Build-to-suit contracts with hyperscalers on 10–20 year leases are very different from shorter-duration, multi-tenant colocation businesses.

What I Am Watching

The Indian data centre market will be a $22 billion market by 2030 by conservative estimates. The IPO pipeline is opening. The hyperscaler money is committed. The power infrastructure is being built. The policy support is there.

The quality of long-term contracts, the power security of specific sites, the promoter credibility, and the balance sheet leverage will matter enormously. But the sector deserves serious attention from every Indian equity investor right now.

The digital highway is being built. The question is not whether to pay attention. It is whether you will act before the traffic arrives.

DISCLAIMER

Twitter/X Profile: @A_Basumallick

For investing in our PMS, drop us a mail at equity@shreerama.co.in

For our research services, visit https://intelsense.in

Subscribe to our free blog https://intelsense.substack.com

DISCLAIMER:

Intelsense.in is owned by Cupressus Enterprises Pvt Ltd (SEBI Registered Research Analyst) with Registration No. INH000013828

Research Analyst or his associates or his dependent family members may hold a financial interest or actual/ beneficial ownership in the financial products/ securities advised herein.

Investment in the securities market is subject to market risks. Read all the related documents carefully before investing.

Shree Rama Managers LLP is a SEBI-Registered Portfolio Management Services Company (SEBI Reg. Number: INP300007341).

Stocks discussed, if any, are for EDUCATIONAL purposes only and should NOT be construed as investment advice.

Please consult your financial advisor and do your own due diligence before investing.