Investor Letter - 2023-24

A look back at the previous year and a peak into this year

For those who prefer video over reading, please view the investor video here:

We have come to the end of the year. All the strategies that we have, have performed well. The market was conducive to the various styles of investment we use.

Choice of Benchmark

The benchmark we use is BSE 500 TRI because we essentially invest across large, mid and small caps so Nifty 50 is not the right benchmark for us. I don’t believe in pigeon-holing investment based on the market cap of companies. No promoter of a company gets up in the morning and decides to operate his company differently because his stock is a large-cap one versus a midcap one.

What we did wrong last wrong

2023-24 was a good year for stocks. In such a year, it is usually the big mistakes of omission that matter more than mistakes of commission. In my entire investing journey of around 24 years now, my biggest mistakes have been not buying a stock after studying it because of some personal bias.

Last year I completely missed the PSU rally. We were perhaps one of the first in Indian markets to have identified the railways theme but other than one private sector company I did not invest in any of the rail PSUs. Ditto for PSU banks as well. Of course, these came into our Quiver/Quant/Hitpicks because of the specific strategy being used. Another big miss last year, which I rectified earlier this year was not having a direct position in the real estate sector in the long-term strategy. I was playing real estate through an ancillary company only.

What went well

When the tide is high, it’s easy to swim. Last year was one such. I always maintain that as an investor our job is to remain invested and the good times will come. The timing of the good time is not certain but what is sure is that it will come.

In the long-term service, our stocks in the railways, infra, engineering, technology, auto ancillary and pharma played out well. I believe that the stocks we own will continue to perform well as businesses and we should be able to reap benefits as investors.

How we see the world now

Fragile geopolitics

The year was fairly volatile. We saw geopolitical risk flare up with wars in Russia-Ukraine continuing for the second year, trouble in Israel-Gaza and continued strife in other regions. Global supply chains are continuously getting disrupted and challenged, with the latest problems coming from the Red Sea where Houthi rebels have attacked more than sixty cargo ships in the last six months. China continues to keep the Taiwan conflict in focus which is one more major flashpoint in world politics at this time.

China+1

US-China relations have been on tenterhooks with both sides sanctioning each other’s commercial interests. The takeaway for global investors is that China has emerged as the main opposition to the US and as such both US and western companies will be forced directly or indirectly to slowly mitigate major dependencies away from China. This China+1 strategy is already underway but will take a very long time to play out. The biggest beneficiary is likely to be the US itself followed by Mexico and then to lesser extent countries like India, Vietnam, South Africa, Indonesia, Malaysia and other smaller Eastern European nations.

India, contrary to the popular belief is within the country, is not an automatic choice for corporates looking for broad basing their sourcing away from China. We still have a long way to go in terms of providing world class infrastructure, facilities or stability in tax regime for global companies to expand in India. We should not be complacent that we are the only alternatives because of our size.

The rise of AI

Perhaps the biggest news item that has captured the fancies of the general public, corporates and investors is the rise of AI. AI has been around for a while but was considered a high-tech thing relegated to research labs. With chatGPT and LLM (large language model) AI has suddenly become mainstream. Common people have now started interacting and getting bowled over by the possibilities of AI.

When any new technology becomes available to the public, it goes through a standard hype cycle.

Today, we are probably somewhere in the uptrend in inflated expectations stage where some like Elon Musk suggesting AGI (Artificial General Intelligence) – AI which can “think” like a human – will be mainstream within a couple of years. That is very unlikely. But what is definitely likely is that like in previous major tech disruptions in our lifetimes – TV, mobile, internet – it will disrupt our daily lives and the way businesses are conducted. How it will impact the IT companies or other businesses is not very evident now but we need to wait and watch this space very clearly.

The transition economy

I am writing this in the first week of April and in Kolkata it is already searing hot with a heat wave going about in the last two days across the state. This is now an expected state of affairs as the effects of climate change become more pronounced. This leads me to the transition economy where India and the world are undergoing a major transition from fossil fuels to renewables. Add the migration of ICE engine vehicles to EVs to this transition economy as well.

India has made three major commitments in this space:

Emissions intensity of 45% below 2005 levels by 2030

50% cumulative electric power installed capacity from non-fossil fuel-based energy resources by 2030

Become net zero by 2070

The installed nuclear power capacity is set to increase significantly, from the current 6780 MW to an impressive 22480 MW by the year 2031. India is to add 18 more nuclear power reactors by 2032 as per NPCIL. India aims to produce 1 lakh megawatt (MW) of nuclear power by 2047, as per Atomic Energy Commission Chairman A K Mohanty.

These goals will drive significant investments in the energy transition economy for the next few years. Similarly, to enable the migration to EVs, setting up new battery plants, charging stations and manufacturing plants will lead to significant capex.

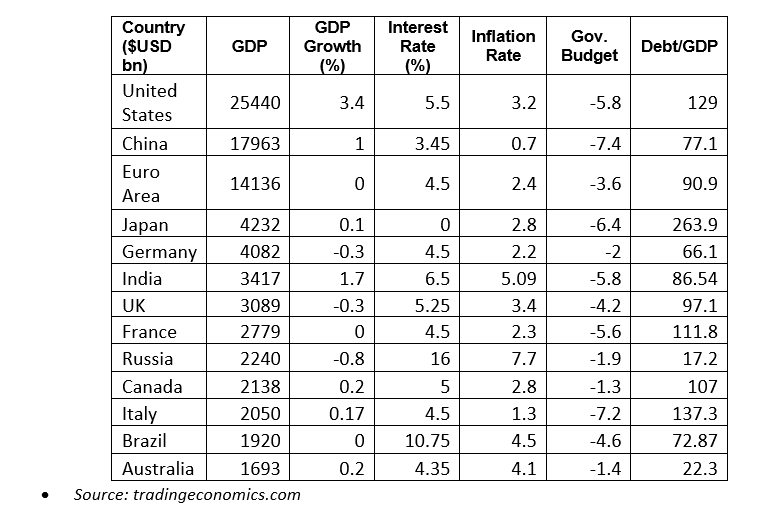

Weak global economy

We are in a global economic weakness. GDP growth across the world is expected to be weak.

India has remained a beacon of hope and driving a significant part of global growth. That should drive significant investments into India over the next few years.

Interest rates are expected to begin to go down, although slowly, in the US, Europe and India. I don’t think there will be any drastic change in rates as central banks would not like to disturb the status quo.

Our strategy

The long-term service is oriented to protect capital and move the portfolio to high-quality businesses. The focus is on compounding wealth over a business cycle.

In Quiver, Q10, Q30 and Hitpicks, our approach is to play short cycles and continue in stocks which are in momentum and also have balance in the portfolio by having a few stocks where we expect a mean reversion by playing turnarounds.

This year could be more volatile than usual with multiple events lined up. The best way to benefit from volatility is by investing regularly. You can continue with or start a SIP account to keep investing regularly.

Thank you for being part of our investing journey.

As always, feel free to reach out to me for any questions or feedback.

Regards

Abhishek Basumallick

Founder, Intelsense

Fund Manager, Shree Rama Managers PMS

DISCLAIMER:

Investments in the securities market are subject to market risks. Read all the related documents carefully before investing.

SEBI Registered Research Analyst - Cupressus Enterprises Pvt Ltd - INH000013828.

Registration granted by SEBI and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.