AR Summary: ICICI Prudential Life - 2022

Here is a short notes cum summary of the annual report. The more we go through annual reports over the years, the better is our knowledgebase about a specific company or industry.

About the Company & its Offerings

ICICI Prudential Life Insurance Co. Ltd (ICICIPRULI) is promoted by ICICI Bank Limited and Prudential Corporation Holdings Limited. Its wholly-owned subsidiary, ICICI Prudential Pension Funds Management Company, distributes products under the National Pension System (NPS) and is a registered pension fund manager.

Began its operations in the fiscal year 2001

Became the first private life insurer to attain an AUM of Rs. 1 trillion

First insurance company in India to be listed on NSE & BSE

Wholly owned subsidiary - ICICI Prudential Pension Funds Management

The company is a registered pension fund manager

It has the following plans under its umbrella –

Non-Linked Insurance Savings Plans- 7 schemes

Protection Plans- 5 schemes

Unit-Linked Insurance Plans- 5 schemes

Group Term Plans- 4 schemes

Pension Plans- 1 scheme

Annuity Plans- 3 schemes

Industry

The life insurance industry offers a variety of long-term savings products across fixed-income and equity platforms.

It also offers annuity, term plans and ‘defined benefit’ health plans. The industry acts as a risk manager by providing a cover against mortality and morbidity risks.

The industry has covered 257 million lives through individual policies and 336 million lives through group policies, providing a total insurance cover (sum assured) of Rs. 236 trillion as of March 2021.

Current Operating Context:

The size of the Indian life insurance sector was Rs. 6.3 trillion on a total premium basis in FY2021, making it the tenth-largest life insurance market in the world and the fifth-largest in Asia.

Out of 24 companies in India, the Life Insurance Corporation of India (LIC) commands a 37% market share based on retail-weighted received premiums, in FY2022.

The top five private life insurance companies together account for another 42% share of the market.

Product Mix:

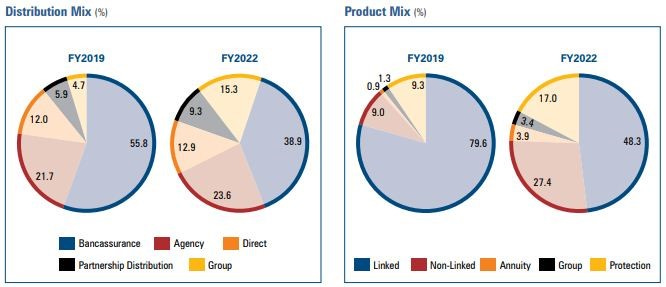

Non-linked products contributed 80% of the new business premium of the industry, primarily driven by LIC.

The private sector saw a further increase in the share of non-linked products to 61% of the new business premium, with linked products contributing the balance during FY2021.

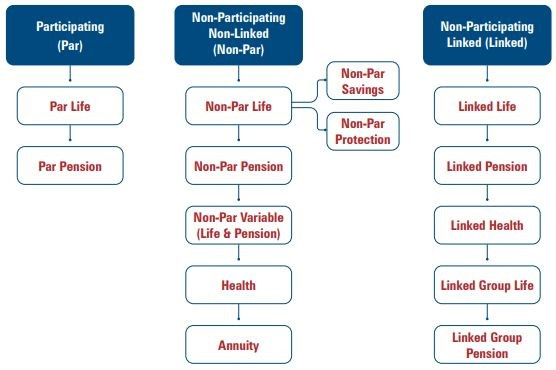

Company Business Verticals

ICICIPRULI’s business verticals can be classified based on products into participating, non-participating non-linked and non-participating linked products.

Key Performance Indicators

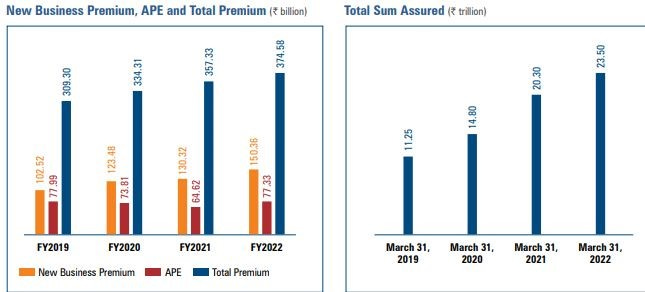

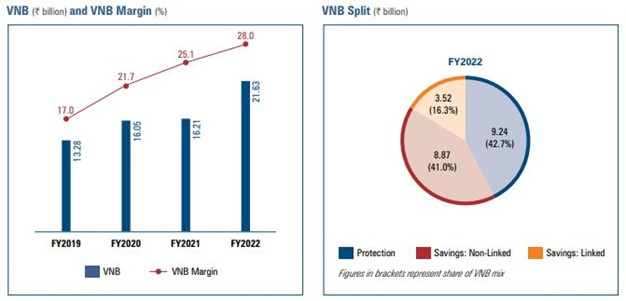

Value of New Business (VNB): Rs. 21.63 bn (up by 33.4%).

Claim Settlement Ratio: 97.8%

Assets Under Management: Rs. 2.4 tn

Total Sum Assured (in-force): Rs. 23.5 tn

Claims Settled: Rs. 312.37 bn.

Business Highlights

Launched an income plan, ‘GIFT Long Term’ which provides customers a guaranteed income for up to 30 years along with life cover.

Launched a return of premium term plan with innovative features such as auto-adjustable insurance cover and one of the most comprehensive and widest financial cover against critical illnesses.

Protection business growth: During the year, saw a further increase in pricing of up to 10% in the retail term products, on the back of increased reinsurance rates.

During the year, ICICIPRULI was the private sector market leader in new business sum assured with our overall market share increasing from 12.5% in FY2021 to 13.4% in FY2022.

Premium Growth:

Annualised Premium Equivalent (APE) grew by 19.7%.

Within product segments, growth rates were as follows:

Annuity: +31.0%

Protection: +25.5%

ULIP: +21.0%

Non-linked savings: +19.2%.

Within channel segments, growth rates were as follows:

Group APE: +48.8%

Direct business: +23.1%

Partnership distribution: +22.0%

Agency: +18.8%

Bancassurance: +10.2%.

Protection business growth: The protection APE grew by 25.5%. The company launched the return of a premium protection product in December 2021 and in the very first quarter of the launch, this variant contributed to 16.9% of the retail protection APE.

Persistency improvement: For FY2022, the persistency ratios for the 13th month and 61st month were stable at 84.6%% and 54.7% respectively.

Productivity improvement: In FY2022 over FY2020, the new business premium grew by about 21.8%, while the increase in expenses was about 20.1%. The APE per employee also increased by 11.1% in FY2022 over FY2021.

Growth Drivers

Aspiration of doubling the FY2019 Value of New Business (VNB) by FY2023 - ended FY2019 with a VNB of Rs. 13.28 billion and for FY2022 it stood at Rs. 21.63 billion with a VNB margin of 28%.

Focus on the growth of the absolute Value of New Business (VNB) through the 4P strategy of Protection focus, Premium growth, Persistency improvement and Productivity enhancement targeted at improving cost ratios.

During the year, the company added 24,607 individual agents and 112 partnerships.

Focus on pension & annuity: The Company would continue to cater to the retirement savings need of customers while managing the investment risk appropriately.

Deepening penetration in under-served customer segments.

To Subscribe to any of our research services, visit https://www.intelsense.in